Just register for the free trial below and we will send you everything you need to evaluate QuickBooks Online including 30-day access, the full 76-page QuickBooks Online Guide (details everything that you can do in the software) plus the video training library. Free end-to-end consultation and support are included so if you need any help along the way, just let us know!

Journal entries are an essential accounting tool used to record financial transactions in QuickBooks Online. They provide a way to manually adjust account balances, record non-standard transactions, and maintain accurate financial records. In this article, we will discuss journal entries in QuickBooks Online, their purpose, how to create them, and common use cases for journal entries in various scenarios.

What are Journal Entries in QuickBooks?

In QuickBooks, journal entries are a method of recording financial transactions that affect the general ledger accounts. Each journal entry consists of a debit and a credit entry, representing equal and opposite changes in different accounts.

In QuickBooks, journal entries are typically used for specific scenarios where other transaction forms or features may not be suitable or available. Here are some reasons to create a journal entry in QuickBooks:

- Manual Debits and Credits: Journal entries allow you to manually enter debits and credits for specific accounts, similar to traditional accounting systems. This can be useful for recording complex transactions or adjustments that cannot be accomplished through standard transactions.

- Transferring Funds: You can use journal entries to transfer money between income and expense accounts or move funds between different types of accounts, such as transferring from an asset, liability, or equity account to an income or expense account.

- Adjusting entries: Journal entries are used to adjust account balances, such as recognizing accrued expenses or adjusting inventory values.

- Correcting errors: When errors are identified in the accounting records, journal entries can be used to rectify them and ensure accurate financial reporting.

- Non-standard transactions: Some transactions, like intercompany transfers, loan repayments, or reclassifications, may not be recorded through the standard transaction forms in QuickBooks. Journal entries provide a way to record these transactions accurately.

Creating Journal Entries in QuickBooks Online

From your QuickBooks Online dashboard, click on +New, and then select Journal Entry under the OTHER column.

Enter the account details in the appropriate debit or credit columns. Make sure the total debits equal the total credits to maintain balance. Provide a memo or description to document the purpose of the journal entry. Select Save and New or Save to record the entry.

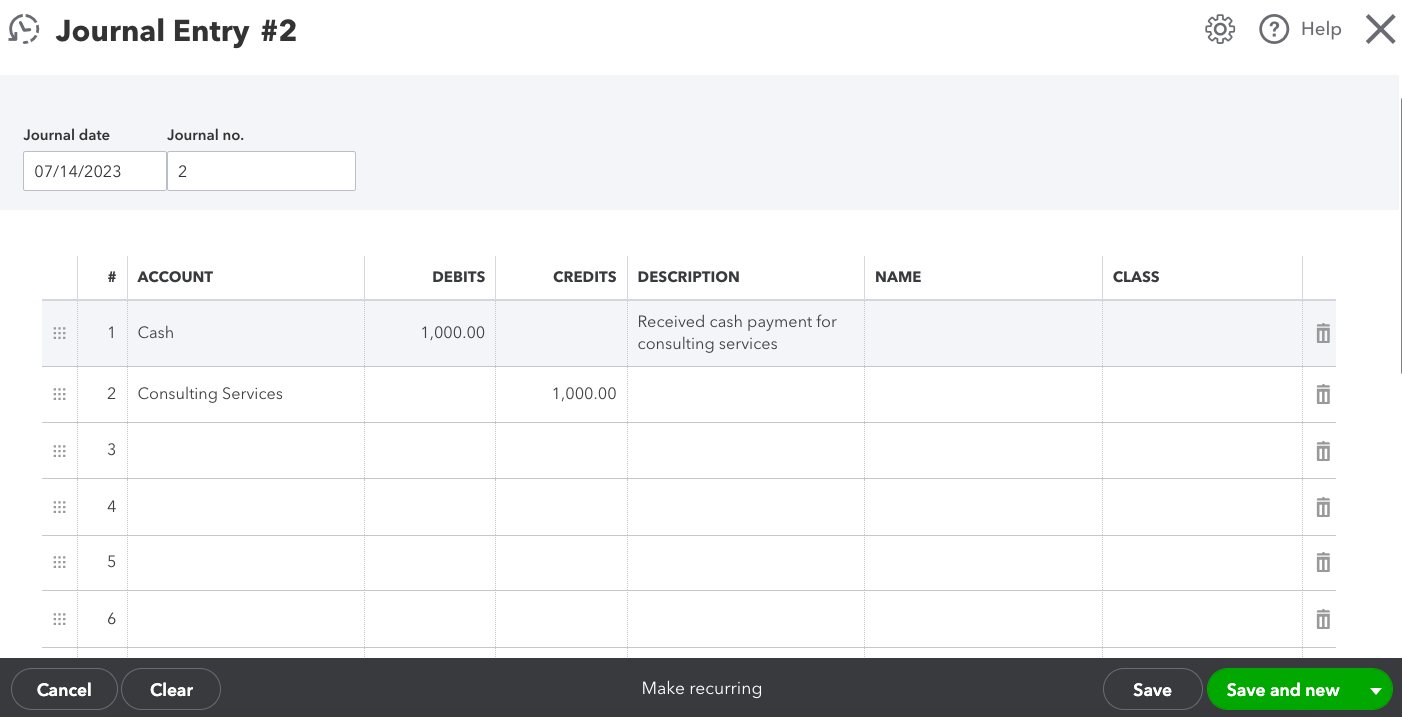

To help you better understand how to complete the form, here’s a sample scenario: Let’s say your business received a cash payment of $1,000 for consulting services provided to a client. You want to record this transaction using a Journal Entry.

- Journal date: Enter the date of the transaction (e.g., July 14, 2023).

- Journal no.: If desired, you can assign a specific Journal Entry number, such as JE001.

- Account: In the first line, select an appropriate account for the debit entry. In this case, select “Cash” from the dropdown list.

- Debits: Enter the amount of $1,000 in the “Debits” column for the “Cash” account.

- Account: In the second line, select the account you want to credit. Let’s assume it’s an “Income” account named “Consulting Services.”

- Credits: Enter the amount of $1,000 in the “Credits” column for the “Consulting Services” account.

- Description: Add a brief description to provide details about the transaction, such as “Received cash payment for consulting services.

Journal entry form in QuickBooks Online

Important Considerations for Journal Entries

- Accuracy: Ensure that the amounts entered in the debit and credit columns are correct and balanced. The total debits must equal the total credits to maintain the fundamental accounting equation (Assets = Liabilities + Equity).

- Account selection: Choose the appropriate accounts to debit and credit based on the nature of the transaction. Understanding the account structure in your chart of accounts is essential for accurate journal entries.

- Supporting documentation: Maintain proper documentation for each journal entry, including invoices, receipts, or any other relevant supporting documents. This helps with audit trails and ensures transparency in financial reporting.

- Reversing entries: In some cases, you may need to reverse a journal entry in a subsequent accounting period. QuickBooks Online allows you to create reversing entries automatically to simplify this process.

Common Use Cases for Journal Entries in QuickBooks Online

- Accruals and deferrals: Journal entries are used to recognize revenues or expenses that have been earned or incurred but not yet recorded through standard transactions. For example, accruing interest expense or deferring revenue for a service to be provided in the future.

- Depreciation and amortization: To allocate the cost of long-term assets or intangible assets over their useful lives, journal entries are used to record depreciation or amortization expense.

- Reclassifications: When transactions are initially recorded in the wrong accounts, journal entries can be used to reclassify them to the appropriate accounts.

- Opening balances: When migrating from another accounting system to QuickBooks, journal entries are used to establish opening balances for accounts, ensuring accurate financial statements.

- Adjusting entries: At the end of an accounting period, journal entries are used to make necessary adjustments, such as recognizing prepaid expenses, estimating bad debt, or adjusting inventory values.

- Intercompany transactions: Journal entries facilitate recording transactions between different entities within the same company. For instance, transferring funds between subsidiaries or recognizing intercompany loans.

For detailed instructions on how to use journal entries in QuickBooks, watch the video below.

Journal entries play a crucial role in maintaining accurate financial records in QuickBooks Online. By understanding their purpose, creating entries correctly, and utilizing them in common scenarios, businesses can ensure accurate financial reporting and make necessary adjustments to their accounts.

Why QuickBooks Online Is a Game-Changer for Small Business Accounting

For small business owners, managing finances can feel like a constant balancing act, trying to stay on...

Can I Use the QuickBooks Online Test Drive to Test integrations?

QuickBooks Online can have a learning curve, especially for new users or businesses trying to integrate...

How Can I Contact QuickBooks Online Support?

Navigating QuickBooks Online can sometimes be challenging, especially when issues arise that require...

How Much Does Each QuickBooks Online Plan Cost per Month?

QuickBooks Online offers a range of subscription plans designed to meet the diverse needs of businesses...

QuickBooks Online Advanced vs Enterprise: A Detailed Comparison

QuickBooks offers two robust solutions for businesses ready to step up from basic accounting software:...

QuickBooks Online vs Desktop: Differences & When to Use Each

QuickBooks, a popular accounting software, offers two main versions: QuickBooks Online and QuickBooks...

Is There a Specific Time of the Month that's Best for Migrating to QuickBooks Online?

Migrating to QuickBooks Online can be a transformative step for your business, offering improved accessibility,...

Can QuickBooks Online Integrate with My Point-of-Sale (POS) System?

Efficient financial management requires seamless integration between your Point-of-Sale (POS) system...

Why Should I Migrate from QuickBooks Self-Employed to QuickBooks Online?

Migrating from QuickBooks Self-Employed (QBSE) to QuickBooks Online (QBO) can significantly enhance your...

How Does QuickBooks Online Handle Sales Taxes?

Managing sales tax is a crucial aspect of running a business. It can be complex and time-consuming, but...

Can I Import My Data From Another Accounting Software to QuickBooks Online?

Transitioning to a new accounting software can seem daunting, especially when considering the need to...

How Does QuickBooks Online Help With Project Management for Marketing Agencies?

QuickBooks Online offers a suite of tools that can significantly enhance project management for marketing...