Just register for the free trial below and we will send you everything you need to evaluate QuickBooks Online including 30-day access, the full 76-page QuickBooks Online Guide (details everything that you can do in the software) plus the video training library. Free end-to-end consultation and support are included so if you need any help along the way, just let us know!

Whether you’re a small business owner, a freelancer, or an accountant, understanding the fundamental accounting terms used in QuickBooks Online is essential for effectively managing your financial records. By familiarizing yourself with concepts such as the chart of accounts, general ledger, accounts receivable (A/R), and accounts payable (A/P), you’ll be able to utilize QuickBooks Online to its full potential.

In this article, we will explain the 10 important accounting terms that you should be familiar with when using QuickBooks Online.

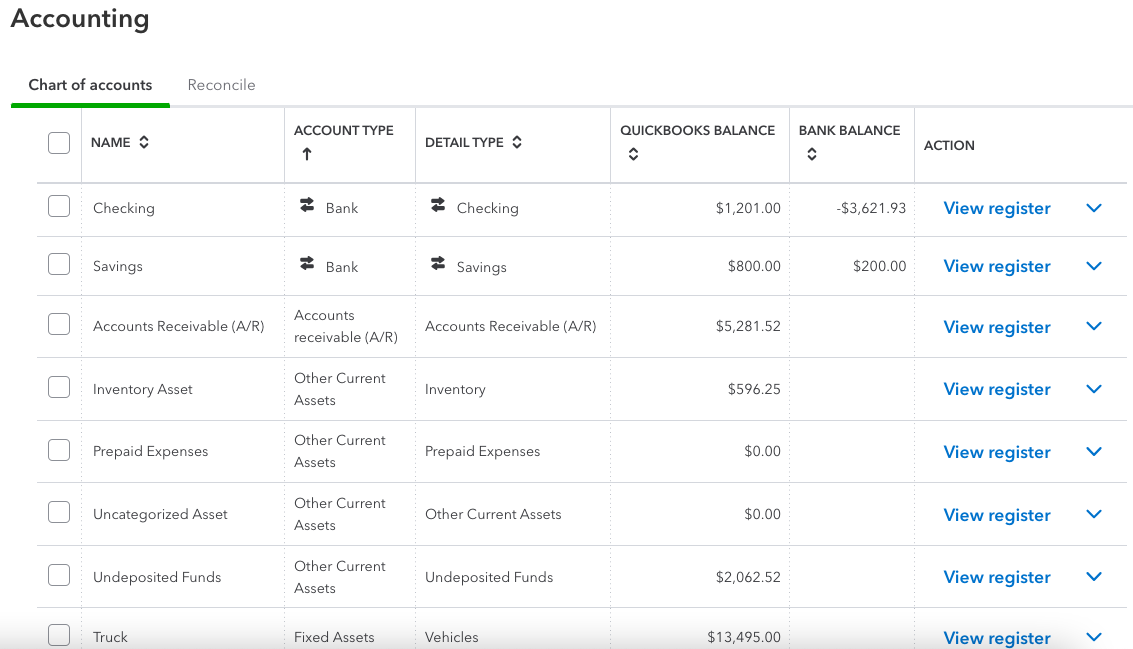

Chart of Accounts

The chart of accounts is a categorized list of all the accounts used in your business’s financial transactions. It includes assets, liabilities, equity, income, and expenses. QuickBooks Online allows you to add, modify, or delete accounts to tailor the chart of accounts to match your business’s unique financial structure and reporting requirements. For instance, to track your income, you may create charts of accounts, such as 4000 Sales, 4010 Service Income, 4020 Interest Income, and 4030 Rental Income.

QuickBooks Online Chart of Accounts

General Leder

The general ledger is the central repository that records all financial transactions of your business. It provides a comprehensive overview of your accounts, enabling you to track and analyze your financial activities effectively. In QuickBooks, the general ledger is automatically generated and updated in real-time as transactions are entered into the system. Each transaction, such as sales, purchases, expenses, and payments, is posted to the appropriate accounts in the general ledger.

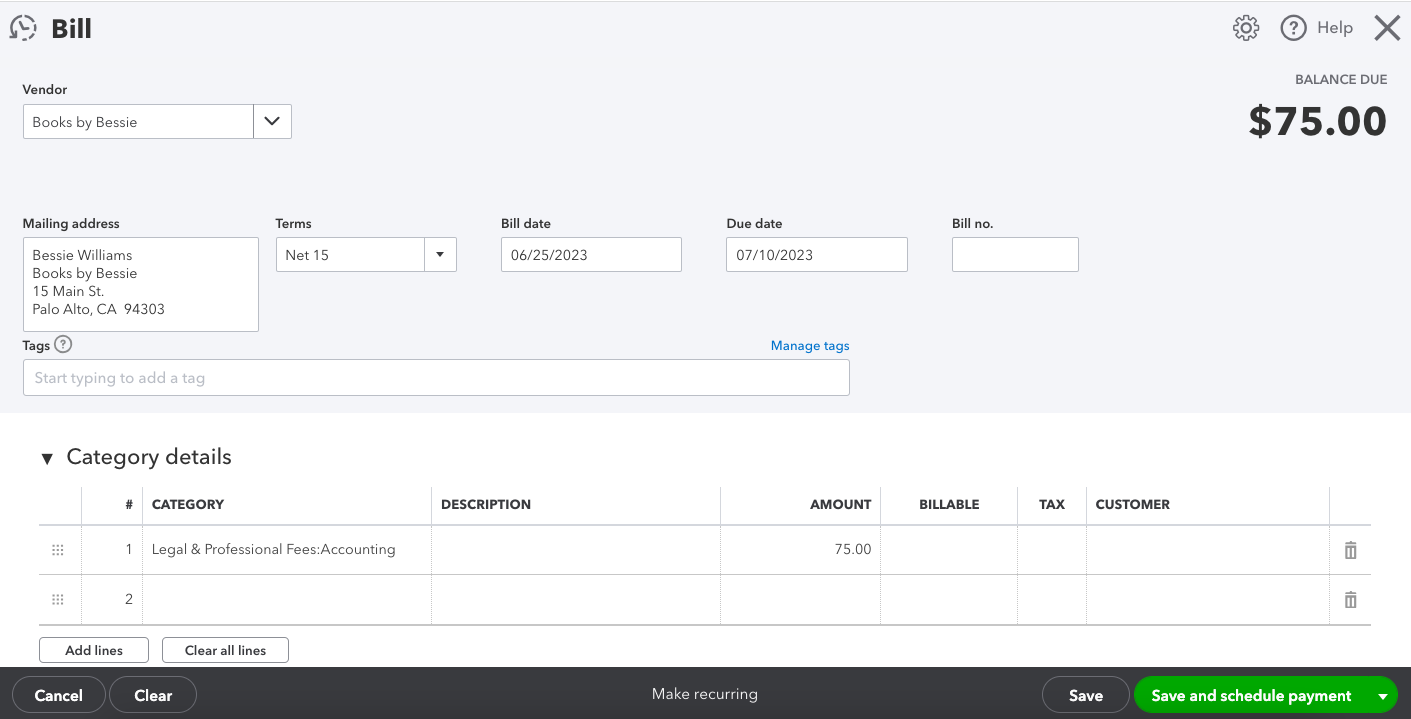

Accounts Payable

Accounts payable in QuickBooks Online represents the money that a business owes to its suppliers, vendors, or creditors for goods or services received on credit. When a business purchases goods or services on credit, it incurs a liability to pay for those items at a later date. QuickBooks Online helps businesses track and manage their A/P efficiently through various features, such as vendor payment, bill entry, bill payment, and A/P aging reports.

Entering a new bill in QuickBooks Online

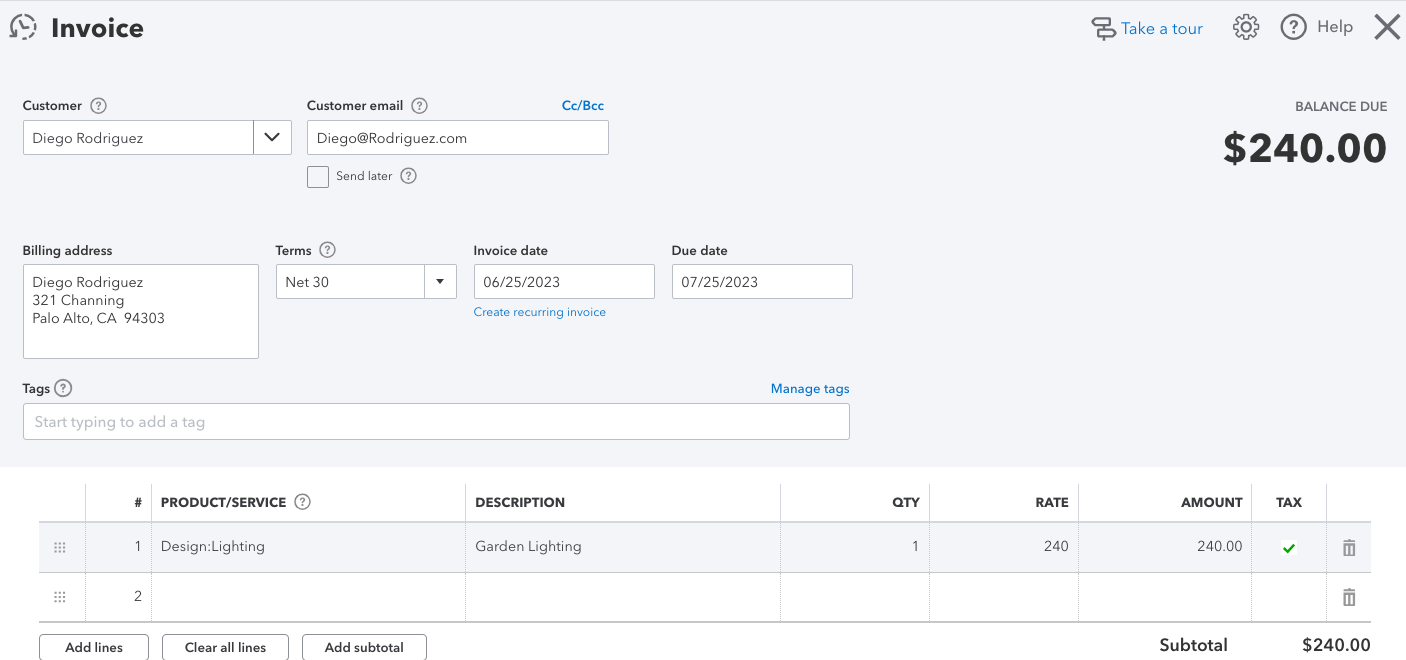

Accounts Receivable

Accounts Receivable in QuickBooks Online represents the money owed to a business by its customers for products or services sold on credit. When a business extends credit to customers, it generates an account receivable that represents the amount the customer owes. QuickBooks offers several features to track and manage A/R efficiently, including customer management, invoicing, payment recording, and AR aging reports.

Entering a new invoice in QuickBooks Online

If you need advanced A/P and A/R features, such as batch invoicing and batch expense entry management, we recommend that you upgrade to QuickBooks Online Advanced.

Bank Reconciliation

Bank reconciliation is the process of comparing and matching your business’s financial records with your bank statements to ensure they align. QuickBooks Online provides a range of banking features to simplify and streamline the bank reconciliation process. For example, the bank feeds feature allows you to connect your bank accounts and credit card accounts directly to your QuickBooks account. This feature automatically imports your bank transactions into QuickBooks, eliminating the need for manual data entry. Bank feeds sync with your bank in real time or on a scheduled basis.

The bank feeds feature matches the imported bank transactions with the transactions you’ve already recorded in your QuickBooks account. It compares the details of each bank transaction with your existing records, such as invoices, bills, and payments, to identify matches. This helps streamline the reconciliation process by reducing the number of transactions that require manual review.

Trial Balance

A trial balance is a report that summarizes the balances of all the accounts in your chart of accounts at a specific period. The purpose of a trial balance is to ensure the accuracy and completeness of your financial records by comparing the total debits and credits of all accounts. By comparing the total debits and credits, you can identify any imbalances or discrepancies that may require further investigation. If the total debits and credits match, it indicates that your accounts are in balance.

Profit and Loss Statement

Also known as an income statement, the profit and loss (P&L) statement provides a summary of your business’s revenues, expenses, and net income or loss over a specific period. The P&L statement provides several benefits to businesses. For instance, it provides insights into the financial performance of the company, indicating whether it is generating a profit or experiencing a loss.

Additionally, the P&L statement helps in financial planning and budgeting by providing a clear picture of income and expenses. It serves as a basis for assessing the financial feasibility of business initiatives, setting revenue targets, and managing costs.

Balance Sheet

A balance sheet is a snapshot of your business’s financial position at a given moment, providing a detailed overview of its assets, liabilities, and equity. It consists of three main sections: assets, liabilities, and equity. The assets section includes current and long-term assets, such as cash, accounts receivable, and property. Liabilities encompass both short-term and long-term obligations, including accounts payable and loans. Finally, equity represents the owner’s or shareholders’ investment in the business, including retained earnings. QuickBooks automatically compiles data from the Chart of Accounts to generate an accurate balance sheet.

Cash Flow Statement

The cash flow statement illustrates the inflow and outflow of cash in your business over a specific period. It categorizes cash flows into operating, investing, and financing activities. The operating activities section captures the cash flows resulting from the company’s core operations, such as revenue generation and day-to-day expenses. The investing activities section focuses on cash flows related to investments in assets, such as the purchase or sale of property, equipment, or investments. Lastly, the financing activities section covers cash flows related to financing the business, such as obtaining loans, issuing equity, or making debt payments.

Journal Entry

In QuickBooks Online, a journal entry is a fundamental accounting tool used to record financial transactions. It is a systematic way to make adjustments or corrections to accounts and ensure the accuracy of the company’s financial records. A journal entry in QuickBooks consists of debits and credits that affect specific accounts based on the accounting principles of double-entry bookkeeping.

Overall, continuously learning and staying updated with accounting principles and best practices in QuickBooks Online will empower you to optimize your financial management processes and maximize the benefits of using this powerful platform.

To further improve your knowledge of QuickBooks Online, watch the video below.

Why QuickBooks Online Is a Game-Changer for Small Business Accounting

For small business owners, managing finances can feel like a constant balancing act, trying to stay on...

Can I Use the QuickBooks Online Test Drive to Test integrations?

QuickBooks Online can have a learning curve, especially for new users or businesses trying to integrate...

How Can I Contact QuickBooks Online Support?

Navigating QuickBooks Online can sometimes be challenging, especially when issues arise that require...

How Much Does Each QuickBooks Online Plan Cost per Month?

QuickBooks Online offers a range of subscription plans designed to meet the diverse needs of businesses...

QuickBooks Online Advanced vs Enterprise: A Detailed Comparison

QuickBooks offers two robust solutions for businesses ready to step up from basic accounting software:...

QuickBooks Online vs Desktop: Differences & When to Use Each

QuickBooks, a popular accounting software, offers two main versions: QuickBooks Online and QuickBooks...

Is There a Specific Time of the Month that's Best for Migrating to QuickBooks Online?

Migrating to QuickBooks Online can be a transformative step for your business, offering improved accessibility,...

Can QuickBooks Online Integrate with My Point-of-Sale (POS) System?

Efficient financial management requires seamless integration between your Point-of-Sale (POS) system...

Why Should I Migrate from QuickBooks Self-Employed to QuickBooks Online?

Migrating from QuickBooks Self-Employed (QBSE) to QuickBooks Online (QBO) can significantly enhance your...

How Does QuickBooks Online Handle Sales Taxes?

Managing sales tax is a crucial aspect of running a business. It can be complex and time-consuming, but...

Can I Import My Data From Another Accounting Software to QuickBooks Online?

Transitioning to a new accounting software can seem daunting, especially when considering the need to...

How Does QuickBooks Online Help With Project Management for Marketing Agencies?

QuickBooks Online offers a suite of tools that can significantly enhance project management for marketing...